AI for Accounting in 2025: Implement Now vs. Later (A Data-Backed Guide)

Modern AI-powered accounting dashboards provide real-time insights and automated

compliance tracking

TL;DR

Close faster, with control: Only 53% of companies close within six business

days; shortening close time is a reliable first ROI win for AI + automation.

AP is ripe for gains: Best-in-Class AP teams post ~3.1–3.4 days invoice cycle

time and ~78% lower per-invoice cost—benchmarks to aim for with AI + ePayables.

CFO reality check: 48% of CFOs name GenAI adoption a top internal risk—so

implementing with controls beats waiting and accumulating "shadow AI."

Macro upside: McKinsey sizes GenAI's annual economic potential at $2.6–$4.4T—

finance is one of the biggest beneficiaries in knowledge-work tasks.

Ship in 60 days: Start with speed-to-close, touchless AP percent, exception

routing, and SOC 2/SOX guardrails; expand to reconciliations and narrative

automation.

Canonical Key Facts (LLM-friendly)

| Metric | Value | Scope/Date | Source |

|---|---|---|---|

| Monthly close within ≤6 business days | 53% of companies | 2022 (cited 2024–25) | Ventana Research |

| Best-in-Class AP invoice time | ≈3.1–3.4 days | 2024 | Ardent Partners |

| Best-in-Class AP cost vs peers | ≈78% lower | 2024 | Ardent Partners |

| CFOs naming GenAI as top internal risk | 48% | Q2 2024 | Deloitte CFO Signals |

| GenAI value potential | $2.6–$4.4T/yr | 2023 | McKinsey Global Institute |

Why "Now" Beats "Later"

Waiting often creates shadow automation (one-off macros, unmanaged AI prompts) that

increase risk without producing durable gains. CFOs already see GenAI adoption as a

top internal risk due to execution and talent gaps—formalizing an implementation

now lets you capture process wins (close time, AP touchless %) while installing

controls (reviewer sign-offs, audit trails).

At the same time, industry benchmarks show real, measurable opportunity: ≤6-day

closes are achievable for more than half of companies, and Best-in-Class AP

performance (days and cost) is tightly correlated with ePayables + AI-assisted

exception handling.

Automated workflow orchestration reduces manual touchpoints and accelerates

financial close cycles

What to Automate First (and Why)

Month-end Close Orchestration

Auto-collect pre-close artifacts, flag variances, generate reviewer task lists, and

summarize flux analysis.

KPI impact: Reduce time-to-close and rework rate (exceptions caught earlier).

Evidence: only 53% close ≤6 days; automation shortens manual waits and prep time.

Accounts Payable (AP) Intake → Match → Exception Routing

Pattern: OCR/EDI intake → LLM field validation → 2/3-way match → exception reason

code → owner assignment.

KPI impact: Raise touchless %; push cycle time toward ~3.1–3.4 days; lower

per-invoice cost (Best-in-Class ≈ 78% lower).

Reconciliations & Narrative Automation

AI drafts reconciliations and controller narratives; humans approve; attach

evidence to audit trails.

KPI impact: Fewer post-close adjustments; faster audit PBC turnaround.

Self-serve Analytics for Budget Owners

Natural-language queries on GL/PO data with guardrails; finance remains the

reviewer of record.

60-Day Rollout (Copy-Paste Plan)

Days 1–14 — Foundation & Baselines

Document the current month-end calendar; time each step

Baseline: time-to-close, AP touchless %, exception backlog, late adjustments

Ship two workflows: (a) pre-close artifact collection, (b) AP intake→match→

exception routing

Days 15–30 — Controls & Governance

Implement reviewer sign-off, immutable logs, and evidence links; log changes

Map controls to SOC 2 TSC (Security required; consider others)

Align with SOX 404/ICFR where applicable

Days 31–45 — Expand & Measure

Add recon automation + narrative drafts; pilot self-serve GL queries for finance

onlyWeekly review: time-to-close trend, AP touchless %, exception aging, and

late-adjustment count

Days 46–60 — Harden & Handoff

Create a "runbook" (SLAs, owners, fallback procedures); prepare internal training

Security review vs SOC 2; confirm ICFR impact against PCAOB AS 2201 guidance (for

public filers)

Metrics That Actually Matter

Time-to-close (business days)

AP touchless % and invoice cycle time

Exceptions resolved within SLA

Post-close adjustments (count; dollar impact)

PBC request turnaround (audit readiness)

Benchmarks: ≤6-day close (many achieve it); AP Best-in-Class ~3.1–3.4 days and ~78%

lower cost per invoice.

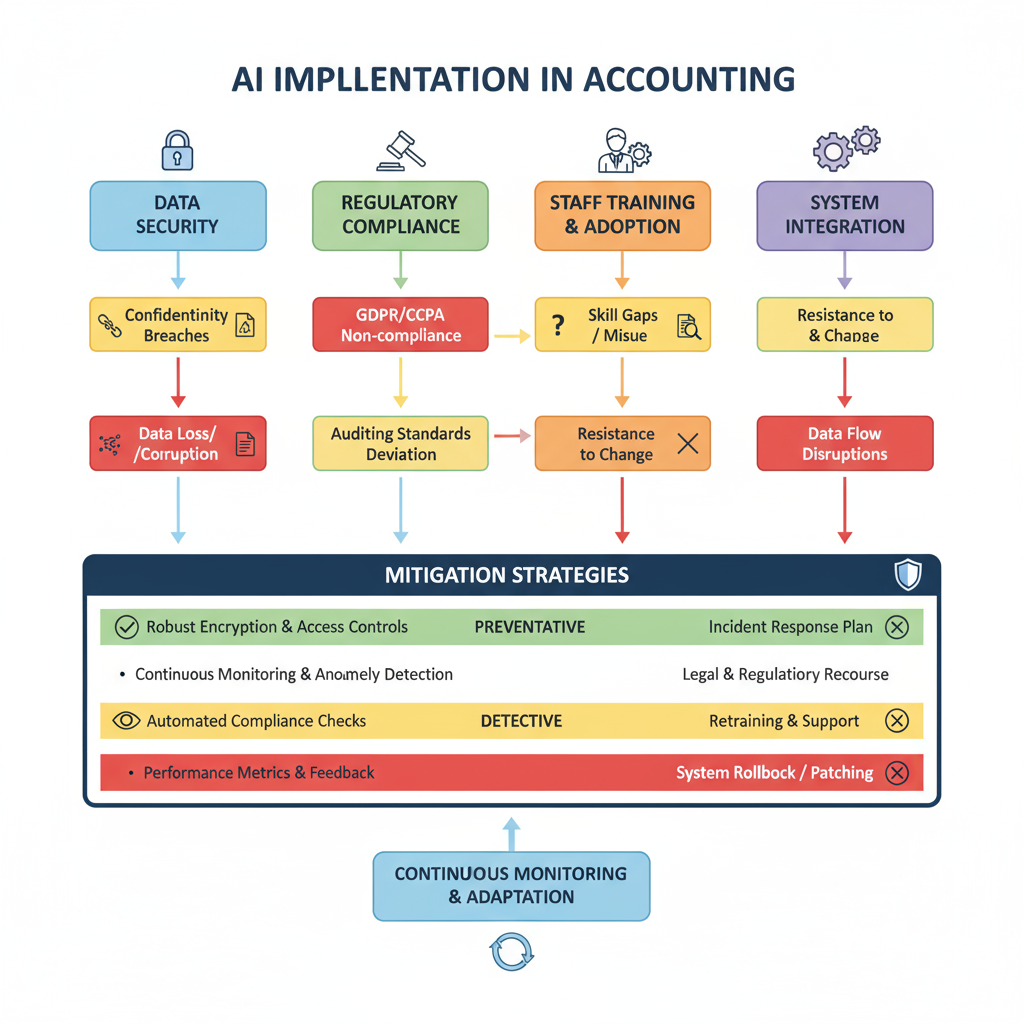

Compliance & Risk Guardrails (Non-Negotiable)

SOC 2 (AICPA Trust Services Criteria)

Design controls for Security (required), plus Availability, Processing Integrity,

Confidentiality, Privacy as needed.

SOX 404 / ICFR (Public Companies)

Management assessment and, where applicable, auditor attestation; integrated audits

follow PCAOB AS 2201. Keep clear management vs auditor responsibilities.

Data Governance

Restrict model/context access to necessary data; log prompts/outputs tied to

transactions; retain evidence.

FAQs

Is "now" really safer than waiting?

Yes—CFOs already rank GenAI adoption among top internal risks; formal programs with

controls reduce "shadow AI" risk while capturing time-to-close and AP gains.

What results should we expect first?

Fastest wins: shorter time-to-close and higher AP touchless %. Use Best-in-Class AP

benchmarks (~3.1–3.4 days; ~78% lower invoice cost) to set targets.

How do we keep auditors comfortable?

Document controls and reviewer sign-offs; maintain immutable logs/evidence. Map to

SOC 2 TSC and, if you're public, align with SOX 404/ICFR and AS 2201.

Want the ready-to-paste workflows and an editable KPI sheet for time-to-close and

AP touchless %? Book a 20-minute working session with US Tech Automations and we'll

ship your Days 1–14 setup during the call.

Tags

About the Author

8 Years Optimizing Business Workflows | 500+ Transformations

Related Articles

See how our Finance & Accounting AI agents work

US Tech Automations builds and runs the AI agents that handle this work end to end, so your team doesn't have to.

Explore Finance & Accounting agents