12,260 Projects Waiting to Connect: U.S. Grid Queue

The USTA Interconnection Queue Index launches today with 12,260 generation and storage projects sitting in the interconnection queues of the U.S. grid operators (ISOs and RTOs) that publish a machine-readable queue — six ISOs and RTOs across 36 states, sealed as of July 9, 2026. This is a census of the published queues, not of every project on every grid in the country, and this launch edition carries no trend claims: every figure below is one sealed snapshot.

One coverage gap is worth naming up front. Nationally, 1,747 projects — 14.2% of the census — carry an unknown status, and that count matches ISO-NE's entire 1,747-project total exactly. That is not evidence those projects are inactive; it means ISO-NE's feed does not publish a status label at all, so every one of its projects defaults to unknown in our count. A queue position, whatever its status, is a request to connect — never a built, approved, or financed project.

12,260 projects are sealed in this census across 6 ISOs and 36 states.

Key Findings

12,260 projects sit across this census's six ISOs and RTOs, spanning 36 states.

Those projects carry 1945.7 GW of proposed capacity, with a median size of 148 MW.

43.6% of all projects nationally have withdrawn; among projects with a known status, that share rises to 50.8%.

14.2% of projects (1,747) carry unknown status — a figure that matches ISO-NE's full project count.

Solar is the leading fuel bucket nationally, with a 33.8% share.

MISO carries more queued projects than any other ISO in this census, at 3,792.

The ISO Leaderboard

| ISO | Projects | Capacity | Median | Withdrawn |

|---|---|---|---|---|

| MISO | 3,792 | 299.5 GW | 150 MW | 56.4% |

| CAISO | 2,278 | 492.2 GW | 128 MW | 77.0% |

| ERCOT | 1,839 | 426.8 GW | 201 MW | 0.0% |

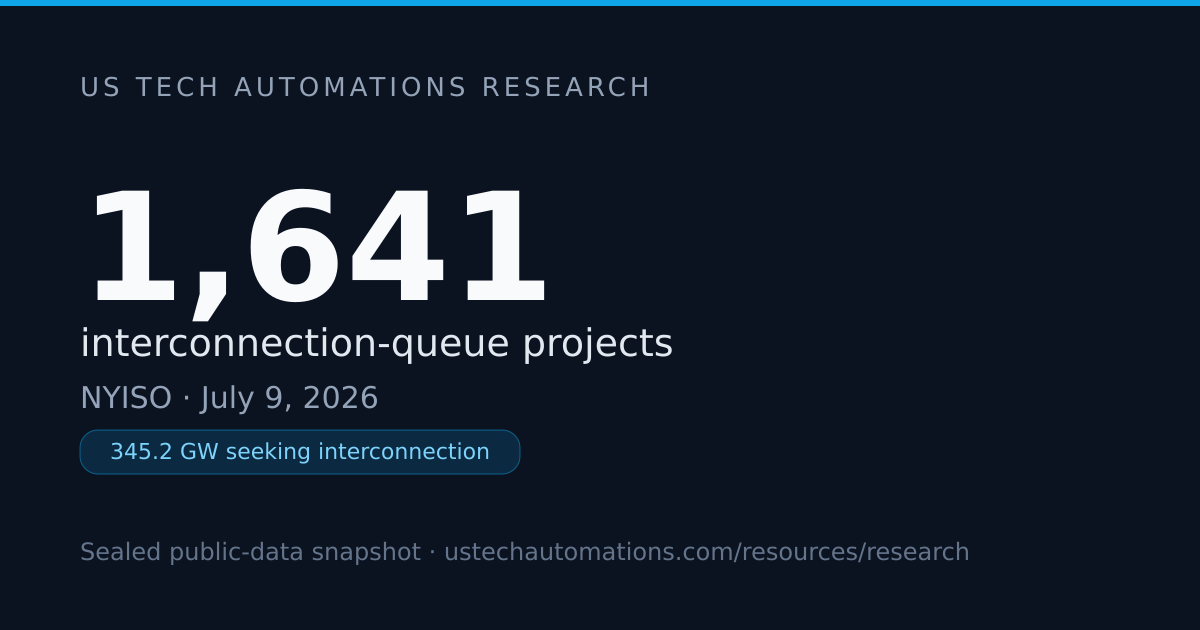

| NYISO | 1,641 | 345.2 GW | 94 MW | 88.3% |

| ISO-NE | 1,747 | 193.1 GW | 26 MW | 0.0% |

| SPP | 963 | 188.9 GW | 173 MW | 0.0% |

MISO carries the most projects of the six, and CAISO carries the most capacity at 492.2 GW despite fewer projects than MISO — a sign that CAISO's average request runs larger. The withdrawn column needs the same caveat everywhere it shows 0.0%: ERCOT, ISO-NE, and SPP all read 0.0% withdrawn in this edition, which is a feed artifact, not a claim that nothing ever leaves those queues. Some ISOs simply drop withdrawn projects from what they publish.

NYISO and CAISO both publish withdrawn projects, and NYISO's 88.3% is the highest of the six — a slice we cover in full in the NYISO interconnection-queue report, including why 97.7% of NYISO's own fuel mix lands in a catch-all Other bucket rather than a real technology reading.

43.6% of every queued project nationally has already withdrawn.

ISO-NE's entire project count — 1,747 — equals the national unknown-status count exactly. Read that as a coverage gap in ISO-NE's own feed, not as a claim that its projects sit idle.

The National Fuel Mix

Fuel and technology labels vary by ISO vendor, so US Tech Automations groups them into six shared buckets by keyword. That bucketing is our methodology choice, and the mapping rules are documented below.

| Fuel / Technology | Projects | Capacity |

|---|---|---|

| Solar | 4,149 | 515,158 MW |

| Battery Storage | 2,826 | 442,540 MW |

| Other | 2,471 | 408,648 MW |

| Wind | 1,720 | 319,023 MW |

| Natural Gas | 555 | 196,076 MW |

| Hybrid | 482 | 53,729 MW |

| Hydro | 24 | 5,086 MW |

| Nuclear | 24 | 2,374 MW |

| Coal | 9 | 3,115 MW |

Solar leads the national queue with a 33.8% share.

Solar and Battery Storage together dominate the top of this table by project count, which lines up with what most industry coverage already says about where developers are putting new requests. The Other bucket sitting in third place, ahead of Wind, is worth a second look before treating it as a real technology signal — as the NYISO report linked above shows, a single ISO's labeling quirks can push a large share of its queue into Other by default, and that same effect contributes to the national Other total shown here.

Which States Carry the Most Queued Capacity

Coverage here traces back to the same six ISOs, so a state's numbers reflect whichever of those ISOs serves it — not every generation project physically located there.

| State | Projects | Capacity | Leading Fuel |

|---|---|---|---|

| California | 2,076 | 416.8 GW | Solar |

| Texas | 2,029 | 453.7 GW | Battery Storage |

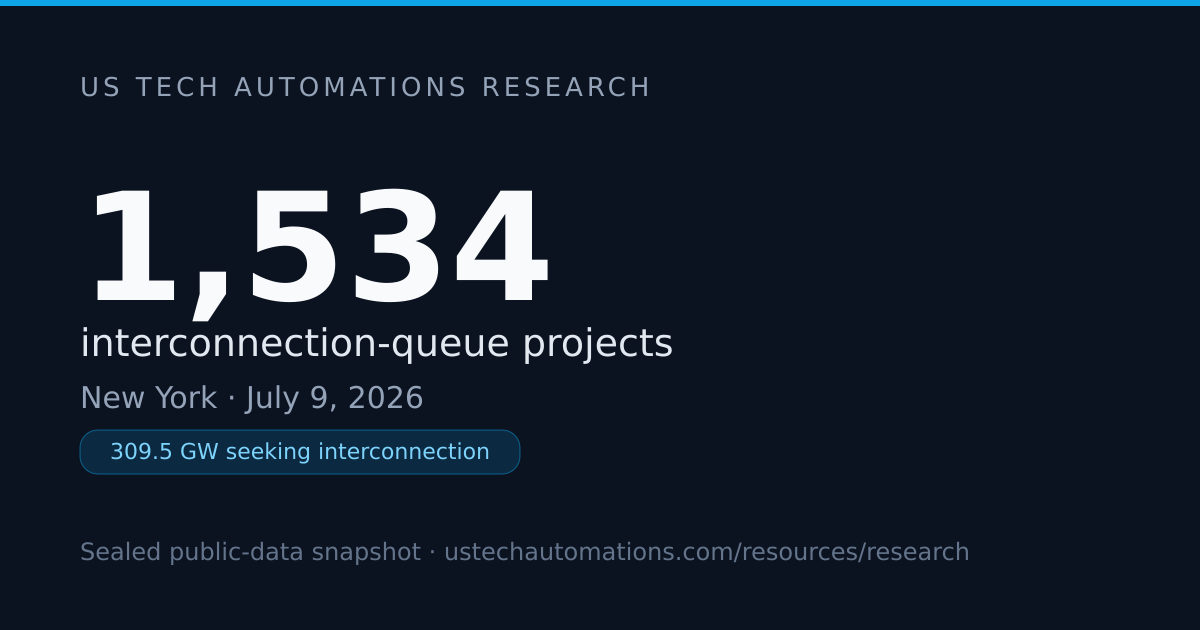

| New York | 1,534 | 309.5 GW | Other |

| Massachusetts | 605 | 81.3 GW | Solar |

| Michigan | 502 | 44.7 GW | Solar |

| Illinois | 482 | 50.6 GW | Solar |

| Indiana | 456 | 39.1 GW | Solar |

| Arkansas | 413 | 32.9 GW | Solar |

| Maine | 407 | 37.0 GW | Solar |

| Louisiana | 392 | 23.7 GW | Solar |

California and Texas are close by project count (2,076 versus 2,029) but Texas carries more capacity (453.7 GW versus 416.8 GW), meaning Texas's average queued project tends to run larger. New York's queue, sitting third by project count, already shows the same Other-fuel pattern seen in NYISO's own report — worth a direct look at that New York state slice if you are working that market specifically. For a state at the opposite end of this leaderboard's visibility, Arizona's much smaller Solar-led queue is a useful contrast in scale.

The Technology Leaderboard

This table adds two things the fuel-mix table above does not show: how often each technology withdraws nationally, and which single ISO holds the most of it.

| Technology | Projects | Capacity | Withdrawn | Leading ISO |

|---|---|---|---|---|

| Solar | 4,149 | 515.2 GW | 45.2% | MISO (1,758) |

| Battery Storage | 2,826 | 442.5 GW | 32.9% | ERCOT (922) |

| Wind | 1,720 | 319.0 GW | 39.1% | MISO (573) |

| Natural Gas | 555 | 196.1 GW | 28.6% | ISO-NE (132) |

| Hybrid | 482 | 53.7 GW | 48.5% | MISO (388) |

| Other | 2,471 | 408.6 GW | 59.0% | NYISO (1,604) |

Other carries the highest withdrawal share of any technology bucket, at 59.0%, while Natural Gas withdraws least, at 28.6%. NYISO alone holds 1,604 of the national Other total — more evidence that a large share of the national Other bucket traces back to one ISO's labeling gap rather than a genuine cluster of hard-to-classify technologies spread evenly across the country.

Methodology

All figures come from public ISO/RTO interconnection-queue listings, via the grid-queue clock (sealed daily, content-hashed). All figures are computed directly from US Tech Automations' sealed daily grid-queue snapshots; nothing is estimated, modeled, or extrapolated. Fuel and status labels are grouped from each ISO's own categories, and the grouping rules appear in the display set.

Coverage here is the ISOs and RTOs that publish a machine-readable interconnection queue — six of them, across 36 states — not every U.S. utility. A utility outside those six ISOs' footprints is simply not represented in this index, and that gap should never be read as "no queued projects there."

Vendor fuel and technology labels differ by ISO and are grouped into Solar, Battery Storage, Wind, Natural Gas, Hybrid and Other by keyword. Each ISO publishes its own status taxonomy; statuses are grouped into withdrawn, operational (explicitly in-service or commercial operation), still-in-queue, and unknown for feeds that publish no status. Some ISOs drop withdrawn projects from their feed entirely.

A queue position is a request to connect, not a built, approved, or financed project. Interconnection queues run heavy on withdrawals everywhere, which is why 43.6% of this entire census — and 50.8% of the projects with a known status — have already withdrawn. This is the index's first edition, so there is nothing to compare it against yet; no growth, surge, or change claim applies until a second sealed edition exists.

Collect. Pull each covered ISO's published interconnection-queue feed daily.

Normalize. Map each ISO's own project, fuel, and status labels into shared fields.

Bucket. Group fuel labels into the six shared technology buckets, and status labels into withdrawn / operational / still-in-queue / unknown, using keyword rules.

Aggregate. Roll the six normalized ISO feeds into one national census.

Seal. Content-hash the aggregated snapshot so every published figure traces back to one immutable daily capture.

Frequently Asked Questions

Q: Does this index cover every U.S. utility's interconnection queue?

A: No. Coverage is the six ISOs and RTOs that publish a machine-readable queue, across 36 states — not every U.S. utility. A utility outside those six is not represented here, which is a coverage gap, not evidence it has no queued projects.

Q: Why does this launch edition have no trend or month-over-month numbers?

A: Because this is the index's first sealed edition. There is no prior snapshot to compare against, so every figure here is a single point-in-time census rather than a change measurement.

Q: What does unknown status mean in this census?

A: It means the source ISO's feed did not publish a status label for that project. Nationally, 1,747 projects (14.2%) carry unknown status, and that figure matches ISO-NE's entire project count — its feed appears not to publish status at all.

Q: Which ISO holds the most queued capacity in this census?

A: By project count, MISO leads with 3,792. By capacity, CAISO leads at 492.2 GW despite fewer total projects, meaning its average queued project runs larger than MISO's.

Q: Who actually uses a national interconnection-queue census like this?

A: Project developers comparing where to file a new request, EPC contractors and equipment suppliers reading regional demand, and utility or policy researchers tracking capacity across ISOs are the most common users of a sealed census at this scale.

Q: Why group fuel labels into six categories instead of using each ISO's own wording?

A: Because every ISO uses different vendor terms for the same technology. Grouping by keyword into Solar, Battery Storage, Wind, Natural Gas, Hybrid, and Other lets this census compare across all six ISOs on shared terms — at the cost of an Other bucket that is sometimes a labeling gap rather than a real technology reading, as NYISO's report shows.

Put This Census to Work

Three groups get direct value from a census this size. Project developers comparing regions before filing a new interconnection request can use the ISO leaderboard above to see where queues already run deep — MISO's 3,792 projects and CAISO's 492.2 GW both signal crowded fields, while SPP's 963 projects suggest more open ground.

SPP carries 963 projects and 188.9 GW — the smallest footprint of the six ISOs in this census, and a useful contrast to MISO's 3,792.

EPC contractors and equipment suppliers reading national demand can watch which technology bucket is growing its still-in-queue share fastest, re-pulling this census on a set cadence rather than reading one sealed day as the whole picture. Energy buyers evaluating power purchase agreements can use the fuel-mix and technology tables together to see where Solar and Battery Storage capacity is actually concentrated versus where the Other bucket is masking the real picture, as it does for New York.

US Tech Automations automates exactly this kind of recurring, cross-ISO monitoring — watching every covered feed for status and fuel changes, then routing the signals that matter to the right team. See how that works for grid and energy teams.

Source: US Tech Automations Research — computed from the sealed daily interconnection-queue snapshot, July 9, 2026.

Get this data as a daily feed

The numbers in this report come from a permit feed we monitor daily. Leave your email and we will follow up about a daily feed for your ZIPs and categories.

Prefer to talk first? Contact us.

Cite this report

US Tech Automations Research, 2026-07 edition. “12,260 Projects Waiting to Connect: U.S. Grid Queue.” https://ustechautomations.com/resources/blog/us-interconnection-queue-index-july-2026

Sealed snapshot sha256: 83af023cf9658e7b563d7b40f5186ff6889c0e5695bfeb5cfa027a2950889a15

Machine-readable data: CSV · JSON · All research & methodology

About the Author

Helping businesses leverage automation for operational efficiency.